[ad_1]

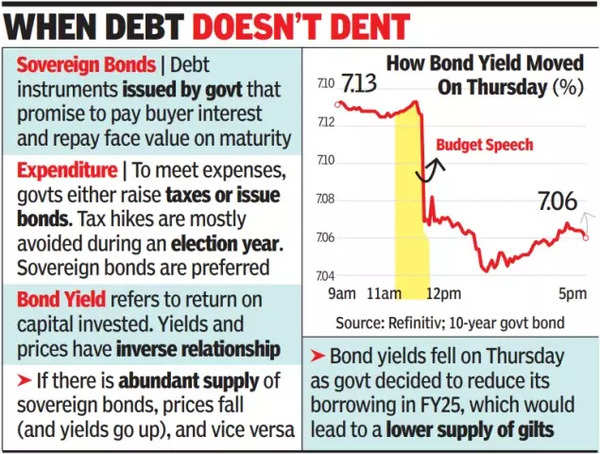

The benchmark yield on 10-year gilts that had closed at 7.15% on Wednesday and was hovering around the same level in early trades on the day of the interim Budget, dropped to the 7.05% level after the FM’s announcements about fiscal deficit and market borrowings for FY25. At the close of the day’s session, the yield on 10-year gilts was at 7.06%, official data showed. The day’s change in yield was the sharpest in nearly 4 months.

In her post-Budget press conference, FM said that govt is on track to meet glide path of below 4.5% fiscal deficit target for FY26.

“This is an anti-inflationary Budget in an election year as the fiscal deficit is reduced from 5.8% to 5.1% (for FY25),” said Murthy Nagarajan of Tata Mutual Fund. “The 10-year yield has come down to 7.05-7.08% levels from 7.15% (on Wednesday). Further drop in yields is expected due to flows from FPIs and expectation of India’s rating upgrade.”

Some of the bond market players and fixed-income fund managers expect RBI to cut rates soon. Along with reduced fiscal deficit numbers and lower market borrowing for the next fiscal, govt has pegged only a moderate growth in the non-capex expenditure, said Pankaj Pathak of Quantum AMC. “This should keep inflation under check and provide enough headroom for RBI to cut interest rates,” Pathak said.

According to a bond fund manager, the rationale behind government‘s fiscal prudence was to rein in the country’s debt-to-GDP ratio, which is now around the 83% level from about 75% in the pre-Covid era. During the pandemic years, running a high level of borrowing was a necessity to cushion the economy from any unwarranted shock. And hence the spike in the debt-GDP reading, the fund manager said.

With the economy now on a relatively stronger footing that is, among other positives, being supported by a high rate of growth of revenue collection, government could now tighten its purse a bit and channelise its investments to the most productive segments of the economy. Also, with the states continuing to run a higher deficit on an aggregate basis, the reduction in central deficit would create some room for them as well, the fund manager said. All these could combine to bring down benchmark yield to the 6.9%-6.85% level by end-FY24, the fund manager said.

[ad_2]

Source link